Originally published August 2019. Updated April 2026 with current Columbus data, 2026 tax rules, and refreshed analysis.

Selling a rental property feels like unlocking value. Sometimes it is. More often, it quietly erases years of compounding returns and hands a meaningful chunk of your equity to agents, title companies, and the IRS. Here are six reasons most Columbus rental owners benefit from holding longer than they planned.

TL;DR

The financial case for holding a rental property long-term is stronger than most owners realize. Mortgage amortization backloads your return into the later years, depreciation recapture and capital gains taxes can reclaim 20% or more of your gain at sale, transaction costs commonly eat 8% to 12% of the sale price, and compounding appreciation of a leveraged asset is one of the most reliable wealth-building mechanics in the U.S. tax code. Selling isn’t always wrong — but most owners who sell a cash-flowing rental regret it within five years.

Key Takeaways

- Mortgage origination costs and principal paydown both reward patience — the longer you hold, the more the math bends in your favor.

- Selling triggers unrecaptured Section 1250 gain (taxed up to 25%) plus long-term capital gains (up to 20%) plus potentially the 3.8% Net Investment Income Tax. Depreciation recapture alone can exceed $10,000 on a typical Columbus rental.

- Transaction costs (agent commissions, title, pre-sale repairs, carrying costs) commonly consume 8% to 12% of the sale price before the IRS takes its share.

- Columbus single-family appreciation has compounded steadily for over a decade, and leveraged appreciation on a property you already own is effectively free.

- The most common reason Columbus owners sell isn’t financial — it’s that managing the property became overwhelming. That’s a solvable problem that doesn’t require liquidating a performing asset.

In This Article

- The Mortgage Math Rewards Patience

- The Tax Bill at Sale Is Bigger Than Most Owners Realize

- The Devil You Know Beats the Devil You Don’t

- Leveraged Appreciation Is Effectively Free Money

- Good Management Makes Ownership Passive

- Transaction Costs Are Bigger Than They Look

- When Selling Actually Makes Sense

- Final Thoughts

- Frequently Asked Questions

1. The Mortgage Math Rewards Patience

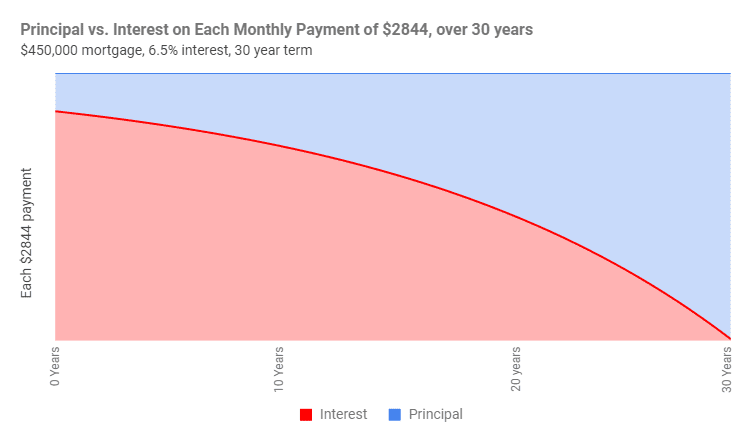

Most rental owners fund their purchase with a 30-year mortgage, and those loans cost several thousand dollars in origination fees up front. Those costs are amortized across the life of the loan, which means the longer you hold, the more years those fees spread across — and the higher your effective return becomes.

But the bigger story is principal paydown. On a 30-year mortgage, the portion of each payment that goes toward principal starts very small and increases every year. In the first year, you might pay down a few thousand dollars of principal on a $250,000 loan. By year 20, you’re paying down $10,000+ per year. Years 25 through 30 are where principal paydown and the subsequent return on equity really accelerate.

The chart above shows a standard 30-year amortization schedule. Notice how the blue principal portion of each payment grows steadily while the orange interest portion shrinks. Sell in year five and you’ve paid mostly interest with little equity to show for it. Sell in year 20, and you’ve built real wealth — wealth that keeps compounding if you keep holding.

The owners who benefit most from rental property are the ones who own long enough to let amortization do its work. The first ten years are the setup; the next twenty are where the real return lives.

2. The Tax Bill at Sale Is Bigger Than Most Owners Realize

Every year you own a rental, the IRS lets you deduct depreciation — an annual paper loss that lowers your taxable income and puts real money back in your pocket. For residential rental property, depreciation is spread straight-line over 27.5 years. It’s one of the best tax benefits in the code.

At sale, the IRS wants some of that benefit back. This is called depreciation recapture, and the rules live under IRC Section 1250. Any gain on the sale that’s attributable to the depreciation you’ve claimed (or could have claimed) gets taxed at a maximum rate of 25% as “unrecaptured Section 1250 gain.” Any remaining gain is taxed at standard long-term capital gains rates — 0%, 15%, or 20% depending on your income. And for many investors, the 3.8% Net Investment Income Tax applies on top of that.

Here’s a Columbus-specific example to make the numbers real.

Example: Clintonville Duplex Sold in 2026

Purchase (2018): $210,000 for a 1920s duplex near Whetstone Park.

Depreciation claimed (2018–2026): Roughly $38,000 at $4,200/year (using a $115,000 building basis, 27.5-year straight-line).

Adjusted cost basis: $210,000 – $38,000 = $172,000.

Sale price (2026): $330,000, reflecting eight years of Columbus appreciation.

Total gain: $330,000 – $172,000 = $158,000.

Tax breakdown at sale:

- First $38,000 (unrecaptured Section 1250 gain) taxed up to 25% = up to $9,500

- Remaining $120,000 taxed at long-term capital gains rate (assume 15%) = $18,000

- Potential 3.8% Net Investment Income Tax on the full $158,000 = up to $6,004

Potential federal tax bill at sale: around $33,500. That doesn’t include Ohio state tax, which adds several thousand more.

You can defer both depreciation recapture and capital gains tax by executing an IRS 1031 exchange — rolling the proceeds into another investment property within strict timelines (45 days to identify, 180 days to close). But a 1031 isn’t a magic eraser; it’s a deferral. The tax liability follows you into the next property and comes due eventually unless you keep exchanging for life. Heirs inheriting the property get a stepped-up basis at your death, which eliminates the embedded gain entirely — another reason long-term holding pairs well with estate planning.

This is general information, not tax advice. Consult a CPA familiar with Ohio rental property taxation before making any sale or exchange decision.

3. The Devil You Know Beats the Devil You Don’t

You know your property. You’ve repaired what needed repairing, you know which tenants are solid, and you have a feel for the maintenance rhythms and the neighborhood dynamics. You’ve paid the tuition on owning this specific asset.

Selling it and buying another property resets that tuition bill to zero. The next property comes with unknown foundation issues, unknown roofing timelines, unknown neighbor conflicts, and unknown tenant histories. Experienced investors know this cost is real, even if it’s hard to put a dollar figure on it.

You don’t buy a rental property. You buy a small operating business. And operating businesses get more valuable once you understand how they work.

4. Leveraged Appreciation Is Effectively Free Money

Columbus single-family home values have compounded steadily for over a decade, and the case for continued appreciation remains strong. Median sale prices across the Columbus & Central Ohio Regional MLS hit $335,000 in March 2026, up 4.7% year-over-year. The 2023 Franklin County Sexennial Reappraisal saw residential values jump an average of 41% metro-wide, with some school districts seeing 60%+ increases. The 2026 Triennial Update is underway right now and will adjust assessed values again this summer.

Here’s the leverage math. If you bought a $250,000 Columbus rental in 2018 with 20% down ($50,000), and the property appreciated to $380,000 by 2026, that’s $130,000 in appreciation on a $50,000 cash investment. Even setting aside rent, cash flow, principal paydown, and tax benefits, that’s a 260% return on the cash you put in — from doing literally nothing beyond owning the property.

Growing net worth through appreciation of a leveraged asset requires no additional effort on your part. The asset grows while you focus on your day job, your family, or your next investment. Sell it, and you trade a compounding asset for a one-time cash event that gets partially taxed away the moment it hits your bank account.

5. Good Management Makes Ownership Passive

Here’s a pattern we see constantly at RLPM: an owner is convinced they need to sell, we dig into why, and the answer usually isn’t financial. The rent still covers the mortgage. The property still appreciates. The tax benefits still flow. What’s actually wrong is that managing the property has become exhausting.

Maintenance calls at 10 p.m. Lease renewals that require three rounds of negotiation. A tenant who stops paying and a landlord who doesn’t know where to start with an eviction. A city inspection notice that needs a response in 10 days. Owning rental property by yourself can turn into a second unpaid job — and the job eventually outgrows what any one owner can sustain.

The solution to “I’m burned out on managing this property” isn’t selling it. It’s hiring someone else to manage it. A good property manager takes the phone calls, coordinates the maintenance, handles the lease renewals and evictions, navigates the Columbus Rental Registry and quarterly inspections, and gives you back your time while the asset keeps compounding in the background.

Warren Buffett made just two visits to the 400-acre farm he’s owned for nearly 40 years. The point isn’t that he’s lazy. It’s that good management lets ownership stay passive — which is how real wealth gets built.

6. Transaction Costs Are Bigger Than They Look

Selling a rental property comes with a cost stack most owners underestimate. On a $330,000 Columbus sale:

- Agent commissions (5% to 6%): $16,500 to $19,800

- Title insurance, escrow, and closing fees (roughly 1% to 2%): $3,300 to $6,600

- Pre-sale repairs and staging: often $5,000 to $15,000 for a rental that’s been occupied by tenants

- Carrying costs during listing and vacancy: 2 to 4 months of mortgage, taxes, insurance, and utilities can easily total $6,000 to $12,000

- Ohio transfer tax and recording fees: a few hundred to a few thousand dollars depending on the county

Add it all up and transaction costs commonly consume 8% to 12% of the sale price before the IRS takes its share. On a $330,000 sale, that’s $26,000 to $40,000 of equity disappearing into the sale process itself.

If you genuinely need access to the equity, a cash-out refinance is often the better path. You keep the asset, you keep the tenant, you keep the tax benefits, and you pull out cash at far lower friction than a full sale. Refinancing into a new 30-year loan also resets the amortization clock (not always ideal, but relevant to underwrite).

When Selling Actually Makes Sense

Holding isn’t always right. Selling can be the correct call when:

- The property no longer fits your investment strategy. Maybe you’ve shifted from cash flow to appreciation, or from single-family to multifamily, and this asset is in the wrong bucket.

- You’re rebalancing a portfolio. Concentrating 80% of your net worth in one Columbus zip code is a risk; selling one asset to diversify is a reasonable response.

- The property is genuinely mispriced in a seller’s favor. If a buyer offers meaningfully above what the fundamentals support, taking the money and 1031-exchanging into something else can make sense.

- Major life changes require liquidity. Divorce, medical needs, inheritance planning, or a move out of state can all legitimately outweigh the hold-it math.

- The asset is structurally broken. Some properties turn out to be persistent money pits — foundation, flood plain, bad zoning, nightmare neighbors. Selling and redeploying capital is the right call for those.

Outside of these scenarios, most owners who sell a performing rental regret it within five years. The equity disappears faster than it ever seems like it should.

Final Thoughts

The U.S. tax code, the mortgage amortization curve, and the mechanics of compounding all line up to reward long-term rental ownership. Transaction costs are real. Section 1250 recapture is real. The devil you know is cheaper than the devil you don’t.

Generational wealth in America has historically been built by owning income-producing assets for decades, not by playing the market. Rental property is one of the most accessible vehicles for that kind of patient capital. The owners who do best aren’t the ones who time sales perfectly. They’re the ones who keep holding.

Bonus: Excerpt from Warren Buffett’s 2013 Annual Letter to Shareholders

Some Thoughts About Investing

“In 1986, I purchased a 400-acre farm, located 50 miles north of Omaha, from the FDIC. It cost me $280,000, considerably less than what a failed bank had lent against the farm a few years earlier. I knew nothing about operating a farm. But I have a son who loves farming and I learned from him both how many bushels of corn and soybeans the farm would produce and what the operating expenses would be. From these estimates, I calculated the normalized return from the farm to then be about 10%. I also thought it was likely that productivity would improve over time and that crop prices would move higher as well. Both expectations proved out. I needed no unusual knowledge or intelligence to conclude that the investment had no downside and potentially had substantial upside. There would, of course, be the occasional bad crop and prices would sometimes disappoint. But so what? There would be some unusually good years as well, and I would never be under any pressure to sell the property. Now, 28 years later, the farm has tripled its earnings and is worth five times or more what I paid. I still know nothing about farming and recently made just my second visit to the farm.

In 1993, I made another small investment. Larry Silverstein, Salomon’s landlord when I was the company’s CEO, told me about a New York retail property adjacent to NYU that the Resolution Trust Corp. was selling. Again, a bubble had popped — this one involving commercial real estate — and the RTC had been created to dispose of the assets of failed savings institutions whose optimistic lending practices had fueled the folly.

Here, too, the analysis was simple. As had been the case with the farm, the unleveraged current yield from the property was about 10%. But the property had been undermanaged by the RTC, and its income would increase when several vacant stores were leased. Even more important, the largest tenant — who occupied around 20% of the project’s space — was paying rent of about $5 per foot, whereas other tenants averaged $70. The expiration of this bargain lease in nine years was certain to provide a major boost to earnings. The property’s location was also superb: NYU wasn’t going anywhere.

I joined a small group, including Larry and my friend Fred Rose, that purchased the parcel. Fred was an experienced, high-grade real estate investor who, with his family, would manage the property. And manage it they did. As old leases expired, earnings tripled. Annual distributions now exceed 35% of our original equity investment. Moreover, our original mortgage was refinanced in 1996 and again in 1999, moves that allowed several special distributions totaling more than 150% of what we had invested. I’ve yet to view the property.

Income from both the farm and the NYU real estate will probably increase in the decades to come. Though the gains won’t be dramatic, the two investments will be solid and satisfactory holdings for my lifetime and, subsequently, for my children and grandchildren.”

Thinking About Selling Because Managing Feels Overwhelming?

That’s the most common reason Columbus owners consider selling — and it’s also the most solvable. RLPM handles maintenance, tenant relations, leasing, evictions, quarterly inspections, and rental registry compliance on 750+ Columbus properties. Flat monthly pricing, $0 leasing fees, live KPI scorecard. Talk to us before you list.

Or get a free rent evaluation · 614.725.3059

Frequently Asked Questions

When should I sell my rental property?

Selling can make sense when the property no longer fits your investment strategy, when you’re rebalancing a portfolio, when a buyer offers meaningfully above fundamentals, when major life changes (divorce, medical needs, out-of-state move) require liquidity, or when the property is structurally broken (foundation, flood plain, persistent major issues). Outside of these scenarios, most owners who sell a cash-flowing rental regret it within five years.

How much will I pay in taxes when I sell a rental property?

You’ll owe unrecaptured Section 1250 gain tax (up to 25%) on the depreciation you’ve claimed, plus long-term capital gains tax (0%, 15%, or 20% depending on income) on any remaining gain, plus potentially the 3.8% Net Investment Income Tax. On a typical Columbus duplex held for 8 years with $38,000 of depreciation and $120,000 of gain, the federal tax bill can approach $33,000 before Ohio state tax. Always consult a CPA before selling.

What is depreciation recapture and how does it work?

Depreciation recapture is the IRS recovering the tax benefits you received from depreciation deductions during ownership. For residential rental property depreciated straight-line over 27.5 years (the required method since 1987), the gain attributable to depreciation is taxed as “unrecaptured Section 1250 gain” at a maximum rate of 25%. This applies whether or not you actually claimed the depreciation deduction — the IRS treats it as “allowed or allowable.”

Can a 1031 exchange help me avoid capital gains tax?

A 1031 exchange defers (not eliminates) capital gains tax and depreciation recapture by rolling proceeds from the sale into another qualifying investment property. You have 45 days to identify replacement property and 180 days to close. The deferred tax liability carries into the new property and comes due when you eventually sell without another exchange. Heirs inheriting the property receive a stepped-up basis at death, which eliminates the embedded gain entirely.

Is Columbus real estate a good long-term hold?

Yes. Columbus has one of the most diversified economies in the Midwest (healthcare, finance, tech, government, education), has added roughly 10,000 residents annually for over a decade, and has seen steady home price appreciation with low volatility compared to coastal markets. The 2023 Franklin County Sexennial Reappraisal saw residential values jump 41% metro-wide, and median sale prices continued climbing 4.7% year-over-year into early 2026.

Should I refinance my rental property instead of selling?

If you need access to equity, a cash-out refinance is usually far more efficient than a sale. You keep the asset, keep the tenant, keep the tax benefits, and avoid 8% to 12% in transaction costs plus the 25% depreciation recapture tax. Refinancing into a new 30-year loan does reset the amortization clock, so model the long-term impact carefully.

What are the total transaction costs of selling a Columbus rental?

Expect roughly 8% to 12% of the sale price. On a $330,000 sale, that’s $26,000 to $40,000 in combined agent commissions (5% to 6%), title and closing fees (1% to 2%), pre-sale repairs and staging ($5,000 to $15,000), carrying costs during listing and vacancy ($6,000 to $12,000), and Ohio transfer tax and recording fees.

How does property management help me avoid selling out of frustration?

A professional property manager handles maintenance calls, tenant relations, lease renewals, evictions, quarterly inspections, rental registry compliance, and emergency response — all the operational friction that exhausts owners into selling. At RLPM, that’s flat monthly pricing starting at $117 per unit, $0 leasing fees, and a live KPI scorecard showing real-time performance metrics for our 750+ managed Columbus properties.

Sources & Suggested Further Reading

- IRS Publication 544 — Sales and Other Dispositions of Assets — Official guidance on Section 1250 and depreciation recapture

- IRS FAQ on Rental Property Sale and Depreciation — Net Investment Income Tax and Section 1250 interaction

- Columbus REALTORS March 2026 Market Update — Current median prices and appreciation trends

- 2026 Columbus Rental Market Update — Full annual investor report with neighborhood data and 2026 outlook

- RLPM Live KPI Scorecard — Real-time performance data for RLPM-managed Columbus properties

RL Property Management Group (RLPM) manages 750+ single-family homes and small multifamily properties across the Columbus metro for long-term investors, accidental landlords, and out-of-state owners. Flat-rate pricing, $0 leasing fees, and transparent live performance data. If you’re thinking about selling because managing the property has become overwhelming, talk to us first. Contact Us Here.