Table of Contents

- Should You Rent or Sell Your Property?

- The Long-Term Wealth Advantage of Renting

- Why People Sell (and why that might be shortsighted)

- What Renting Looks Like for Different Types of Property Owners

- The Hidden Math: Cash Flow Isn’t the Whole Picture

- Use the Calculator to Get Real Answers

- Ready to See What Your Property Could Really Do?

Should You Rent or Sell Your Property? Let’s Talk It Through

Should You Rent or Sell Your Property? Let’s Talk It Through

You’ve got a property. Maybe you’re moving, maybe you inherited it, or maybe you’re just weighing your options. Either way, you’re standing at a financial fork in the road: Should I rent this place out, or just sell it and move on?

That’s a big question—and a smart one to ask.

Selling is tempting. It’s clean, quick, and gives you a lump sum of cash you can use right away. No tenants. No maintenance. No monthly ups and downs. Just a check, deposited, done.

But that short-term relief can come at the cost of long-term opportunity.

What many owners don’t realize is that renting out your property, especially with a solid management team in place, can build far more wealth over time than selling ever could (even if the numbers feel a little tight right now).

This isn’t a pitch. It’s a perspective shift.

We’ve seen this play out over and over again in the Columbus market. People who choose to hold and rent almost always come out ahead over a 5, 10, or 20-year timeline. They build equity, enjoy tax benefits, and unlock a steady stream of income that just keeps growing.

And the best part? You don’t have to guess.

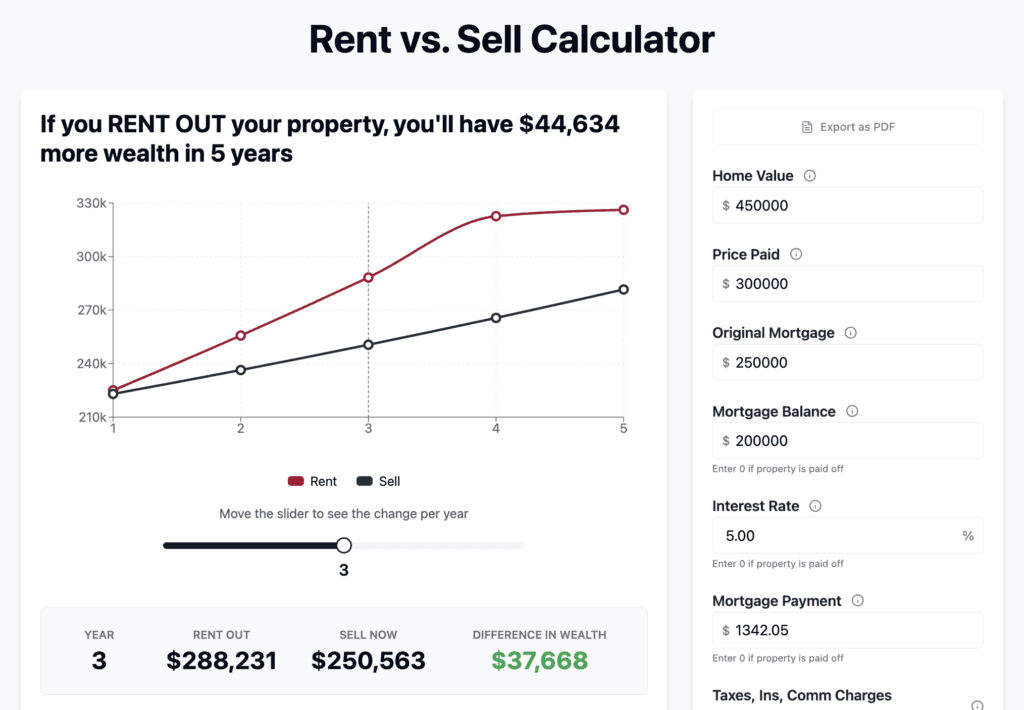

We built a free Rent vs. Sell Calculator that gives you a detailed, side-by-side comparison based on your actual numbers. It shows how much wealth you’d likely build by renting out the home versus selling it now and investing the proceeds.

But before you plug in your info, let’s walk through why renting might make more sense than you think—especially if you’re playing the long game.

The Long-Term Wealth Advantage of Renting

Here’s the truth: long-term real estate wins aren’t built on instant cash flow—they’re built on time, leverage, and appreciation.

Even if your monthly profit is break-even (or even slightly negative), you’re still gaining value in three powerful ways:

- Your tenants are paying down your mortgage.

- Every month, a portion of your loan gets paid off by someone else.

- Your property is (likely) appreciating.

- Over the past 10 years, Columbus home values have trended upward. Holding means capturing that growth.

- You’re gaining tax advantages.

- Rental properties come with deductions: mortgage interest, depreciation, repairs, insurance, and more.

This trio—equity paydown, appreciation, and tax sheltering—creates what we call wealth layering. It’s the slow, steady growth that turns one home into a real financial asset.

Compare that to selling: once it’s gone, it’s gone. Sure, you get a lump sum—but now you’re out of the game. You’ve given up a long-term appreciating asset in exchange for short-term liquidity.

And if you reinvest those sale proceeds elsewhere, will the return be as consistent or tax-advantaged? That’s the question.

Renting isn’t about short-term wins—it’s about building something that grows and compounds. It’s about creating options.

Even if your current monthly income is slim, the overall wealth you’re building behind the scenes can be substantial. That’s what makes real estate so powerful—and why holding onto your property might be the smartest financial decision you make this decade.

Why People Sell (and why that might be shortsighted)

We get it. Selling has its appeal:

- You get a lump sum of cash.

- You avoid the work and stress of being a landlord.

- You can “move on” without lingering responsibilities.

And for some owners, that’s the right choice—especially if you’re strapped for cash, overwhelmed by the idea of managing a rental, or simply ready to close the chapter.

But it’s important to look at the full picture before you sell.

Here’s what selling can really mean:

- You’re exiting an appreciating market.

- Columbus has seen consistent home value growth. Selling now might mean missing out on another 10+ years of gains.

- You’ll pay to sell.

- Realtor commissions (5–6%), closing costs, and repairs add up—cutting deep into your net proceeds.

- You give up passive income potential.

- That monthly rent check? Gone. So is the long-term payoff of a tenant helping pay off your mortgage.

- You might mistime the market.

- Selling during a dip can lock in losses. Holding gives you time to wait for better conditions.

- You lose future flexibility.

- Once you sell, it’s hard to get back in—especially with rising home prices and higher interest rates.

So if you’re considering selling purely to simplify things, ask yourself: Are you solving a short-term discomfort by giving up long-term gains?

That’s where professional property management comes in. You don’t have to be the one dealing with tenants, maintenance, or compliance. Renting doesn’t have to be hard. You just need the right team behind you.

And the results? They’re often more rewarding than you expect.

What Renting Looks Like for Different Types of Property Owners

Every owner’s situation is different. But in nearly every case, renting opens the door to long-term gains—without the stress of doing it all yourself. Here’s how it plays out for different types of owners we work with:

For the Accidental Landlord

Your situation: You inherited a property or relocated for work. You didn’t plan to be a landlord, and managing a rental sounds stressful or risky.

Why renting still works:

- You keep the property in the family, while it earns passive income.

- A professional property manager handles everything from tenant placement to maintenance.

- Even modest rent today adds up to real wealth in 10 years.

Renting doesn’t have to mean being “on call.” With the right support, it can feel more like owning a low-effort financial asset.

For the First-Time Investor

Your situation: You just bought your first rental (or are thinking about it). You’re excited but unsure what to expect.

Why renting still works:

- You’re building long-term equity from day one.

- The upfront costs (repairs, turns, etc.) are investments, not losses.

- Professional management helps you avoid costly mistakes early.

Think of this as planting the first tree in your rental forest. The earlier you start, the better the long-term growth.

For the Small Portfolio Owner

Your situation: You own 2–5 rentals, maybe self-manage, and you’re juggling a full-time job. You’re wondering if it’s all worth it.

Why renting still works:

- Outsourcing management gives you back your time.

- Holding allows you to grow your portfolio without burnout.

- Property value gains + consistent rent = strong returns over time.

This is the stage where scaling gets real. Renting through a management partner sets you up to go from 3 doors to 10—without losing your weekends.

For the Out-of-State Investor

Your situation: You bought in Columbus but live elsewhere. Managing from afar feels risky, and selling sounds simpler.

Why renting still works:

- With boots-on-the-ground support, you don’t need to live nearby.

- We handle everything from tenant communication to maintenance.

- Columbus remains a high-potential market—why exit now?

Many of our clients in this category build entire Columbus portfolios from afar. It works—if you’ve got the right team.

For the Long-Term Investor

Your situation: You’ve been in the game for years. You think like a business owner and want your capital working for you.

Why renting still works:

- Selling may feel like a reset—but it can stall portfolio growth.

- The numbers often show stronger ROI from holding + leveraging equity.

- A trusted PM helps you operate like a true investor: efficient, data-driven, and hands-off.

For you, renting isn’t emotional. It’s strategic. We help maximize the returns—and minimize the friction.

The Hidden Math: Cash Flow Isn’t the Whole Picture

When owners look at rental property performance, the first question is usually:

“What’s the monthly cash flow?”

That’s fair. But it’s only one piece of the puzzle.

A low—or even negative—cash flow today doesn’t mean a rental is a bad investment. In fact, many properties that barely break even on paper are quietly building wealth in ways that don’t show up in a simple rent-minus-expenses equation.

Here’s what often gets overlooked:

- Loan Paydown – Each mortgage payment reduces your loan balance, increasing your equity.

- Appreciation – If your property gains value over time, your net worth grows—even without strong monthly income.

- Depreciation & Tax Benefits – You can write off a portion of the property’s value each year, reducing your taxable income.

When you combine those three factors, the overall return is often substantially higher than the monthly cash flow might suggest.

Think of it this way: renting is a long game.

If you’re only evaluating based on month-to-month income, you’re missing the bigger win—total wealth creation. And the longer you hold, the more these benefits compound.

That’s why our Rent vs. Sell Calculator looks beyond simple cash flow. It factors in equity growth, taxes, appreciation, and reinvestment returns—giving you a true side-by-side wealth projection.

Use the Calculator to Get Real Answers

Decisions like this are too important to make based on gut feeling alone. That’s why we built the Rent vs. Sell Calculator—a free, data-driven tool that shows you the actual math behind both options.

In just a few minutes, you’ll see:

- Projected cash flow and expenses over time

- Your property’s expected appreciation and equity growth

- Total wealth accumulation from renting vs. selling

- How reinvesting your sale profits might stack up

You can even adjust advanced variables like:

- Occupancy rate

- Make-ready and capital improvement costs

- Management fees

- Tax rates

- Mortgage details

This is about clarity, not guesswork. Once you run the numbers, it’s easier to make a confident, informed choice.

And if the calculator confirms that renting is the better path? Even better. We’re here to help you execute it with less stress and better returns.

Ready to See What Your Property Could Really Do?

If you’re on the fence about whether to rent or sell, don’t make the call in the dark.

Use our Rent vs. Sell Calculator to get real answers. No guessing. No pressure. Just clear insight into what each path looks like for your property.

And if the numbers lean toward renting—but the idea of managing tenants or repairs stresses you out? That’s where we come in.

RL Property Management offers full-service solutions for owners who want the returns of real estate without the daily headaches. We handle everything—leasing, maintenance, compliance, communication—so you can stay focused on your life, your business, or your next investment.

Run your numbers. Then let’s talk.

Try the Calculator or Schedule a Consultation with our team today.

Not sure what your property could rent for? We can help you out there, too. Start with a free rent evaluation, then plug the results into the rent vs. sell calculator.